The equation of exchange shows the relationship between the money supply, velocity of money, price level, and real GNP. This equation is a tautology that no competent economist would argue against.

Money-supply * Velocity-of-money = Price-level * Real-GNP

On the scale that we are currently increasing the money supply, the real GNP is basically constant. Inflation can be thought of as too much money chasing too few goods. When looking at a 400% change in the base money supply over the last 5 years, the change in real GNP (change in goods) is so small that we won't be off much by ignoring it. To help understand this short period of time with a big change in the base money supply, we can make a simplified version of the equation of exchange.

Money-supply * Velocity-of-money = Price-level * constant

If the velocity goes down as the money supply goes up, it is possible to increase the money supply without changing the price level.

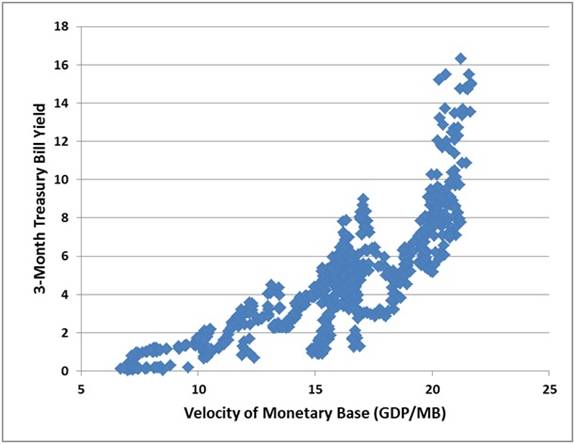

Hussman has shown that as interest rates go down the velocity of money goes down and as interest rates go up the velocity of money goes up.

At first when the Fed makes new money and buys bonds, they increase the price of bonds, which means they lower the interest rate. Hussman's data shows this lowers the velocity of money. The lower velocity can compensate for the increased quantity of money so that often new money does not cause inflation right away.

The equation of exchange can be used with whichever definition of money supply you want to use (base money, M1, M2, etc). It is most clear that inflation will come if we use base money as our definition of the money supply. The base money supply has gone up by around a factor of 4 in about 5 years.

Since we have so far avoided inflation, the velocity of base money must have gone down by about a factor of 4 during this same period. The way this happened is that most of the new base money the Fed has made has just sat still in the Fed as excess reserves. This huge amount of non-moving money lowers the overall average velocity of money. If you think about it, it makes sense that making new money that does not leave the Fed should not cause inflation. Paying higher interest on excess reserves than short term bonds were paying was Bernanke's great new trick to hide a few trillion dollars out in the open.

However, now interest rates are going up. From Hussman we should now expect the velocity of money to go up. From the simplified equation of exchange, when the velocity of money and the money supply are both going up we should expect inflation.

As interest rates return to normal levels, the velocity of money will also return to normal levels. Then we will have 4 times the money supply and a normal velocity of money. By the simplified equation of exchange, we will then have 4 times the price level. We will have very high inflation.

You may be wondering, "why can't the Fed hold interest rates down forever?". Good question. If inflation is higher than the interest rate, then everyone and their brother can make money by borrowing and buying random stuff. To hold rates down the Fed would have to make an ever increasing amount of money, resulting in ever increasing inflation and ever increasing borrowing. The Fed seems interested in tapering their money creation which will mean letting interest rates go up. Japan, at least for the moment, seems to have chosen to try to hold interest rates down no matter how much money creation it takes. Once government debt and deficit are out of control, there is no good path for the central bank.

For the velocity of money to return to normal, it is reasonable to expect the excess reserves at the Fed will enter the real economy. There are those who think these excess reserves are somehow trapped but a bank with excess reserves can send an armored truck to the Fed and withdraw paper Federal Reserve Notes with no restrictions on them. This could happen at any time and possibly very suddenly. A couple trillion dollars suddenly flowing into the real economy would clearly result in high inflation.

Even Krugman has said that increasing the money supply is only safe when interest rates are near the zero lower bound. With interest rates going up, even by Krugman's logic, we should expect inflation.

Here is another way to look at it. From 1913 to 2007 the Fed made about $800 billion in new money total. Since then it makes around that much each year. Nearly 94 years worth of money every 12 months. In this environment, one should expect to see "too much money chasing too few goods".

Another way to look at it. In order to not cause inflation the central bank would need to be able to withdraw all the new money they created. There is just no way this can happen. Interest rates would shoot up, the value of the bonds the Fed held would crash, and they could not sell them for enough to withdraw as much money as they created.

High inflation will come. It is just a question of when.

Prize for historical example of 4x on monetary base and low-inflation

There are more than 100 cases where rapid monetization seems to have resulted in hyperinflation (using 26% cutoff). I am looking for one good example where it did not.I will pay $100 US by paypal to the first person to comment below about a case where a central bank increased the monetary base by a factor of 4 or more by buying government bonds in 5 years or less and did not get at least double digit inflation sometime during that time or the 5 years after. Must provide links to reliable info on base money growth and subsequent inflation.

This has to be for an established central bank, not a new one or a new currency at an old one (currency and bank around for at least 10 years prior to 4x period). It must be expanding the monetary base by buying up government bonds for that country (like US, UK, and Japan are doing). I am looking for a situation where a central bank did something similar to what the US has done in the last 5 years but that did not get high inflation.

Note one round of this has been won as of 1/5/14 (see comments) but I had not specified that the 4x expansion had to be from monetization which is in the current rules.

All

it would take is for one case where the equation of exchange did not

work. One time where the interest rates and inflation rates went up

substantially but the velocity of money did not. One historical case

where a central bank bought up half of a government debt that was more

than 100% of GNP, using new made money, without getting serious

inflation in the next 10 years. Maybe that is your answer, 10 years.

But I don’t think it has ever happened in history and there are many

many many times where lots of new money caused inflation down the road.

You have to think “this time is different” to not expect inflation at

some point. Doubt it very much.

Read more at http://pragcap.com/my-favorite-posts-from-2013#p4TCJp3CbFyzp1OI.99

Read more at http://pragcap.com/my-favorite-posts-from-2013#p4TCJp3CbFyzp1OI.99

All

it would take is for one case where the equation of exchange did not

work. One time where the interest rates and inflation rates went up

substantially but the velocity of money did not. One historical case

where a central bank bought up half of a government debt that was more

than 100% of GNP, using new made money, without getting serious

inflation in the next 10 years. Maybe that is your answer, 10 years.

But I don’t think it has ever happened in history and there are many

many many times where lots of new money caused inflation down the road.

You have to think “this time is different” to not expect inflation at

some point. Doubt it very much.

Read more at http://pragcap.com/my-favorite-posts-from-2013#p4TCJp3CbFyzp1OI.99

Read more at http://pragcap.com/my-favorite-posts-from-2013#p4TCJp3CbFyzp1OI.99

All

it would take is for one case where the equation of exchange did not

work. One time where the interest rates and inflation rates went up

substantially but the velocity of money did not. One historical case

where a central bank bought up half of a government debt that was more

than 100% of GNP, using new made money, without getting serious

inflation in the next 10 years. Maybe that is your answer, 10 years.

But I don’t think it has ever happened in history and there are many

many many times where lots of new money caused inflation down the road.

You have to think “this time is different” to not expect inflation at

some point. Doubt it very much.

Read more at http://pragcap.com/my-favorite-posts-from-2013#p4TCJp3CbFyzp1OI.99

Read more at http://pragcap.com/my-favorite-posts-from-2013#p4TCJp3CbFyzp1OI.99

It seems to me like your second equation

ReplyDeleteMoney-supply * Velocity-of-money = Price-level

should be written

Money-supply * Velocity-of-money = Price-level * constant.

Many of us agree that the price-level should expand when the money supply (MS) increases. The entire QE program seems to be based on this premise. The surprise is that real GDP HAS stayed nearly constant!

The performance of this equation begs for explanation. One suggestion is that the increased money-supply is going into very few hands, hands that are savers who will spend at an unknown time in the future.

If the increase in MS is indeed going into the hands of savers, who are these savers? When might they begin spending the increased MS with the expected increase in velocity? I have only guesses for answers to those two questions.

Yes, it is probably more clear putting in "constant" so I have made that change. Thanks.

ReplyDeleteI think the explanation for why we have not had inflation can be done with the low velocity because $2.4 trillion is sitting still at the Fed. You could also look at it as the Fed made the money but then kept it inside the building so nobody has actually used it. Either way, when the excess reserves stop increasing, or start going out of the Fed, then we should expect inflation. With interest rates going up I would expect that to start happening.

"You could also look at it as the Fed made the money but then kept it inside the building so nobody has actually used it."

DeleteIt's used: by the commercial banks to clear payments, amongst other things. For example, some gets transferred to Treasury's Fed deposit account when taxes are paid or the Tsy sells bonds. Also, just sitting there it gets tallied as bank assets and helps them meet their capital requirements (and reserve requirements too of course, which they are in no danger of not meeting currently). It comes back to the banks when Tsy spends. Some gets destroyed when banks buy paper reserve notes (and it's created if the notes are sold back to the Fed).

"when the excess reserves stop increasing, or start going out of the Fed"

Only way "out of the Fed" is if the banks buy cash (reserve notes) from the Fed. Then the electronic reserves are destroyed and replaced with the cash, so they never really leave the banks' possession (by definition), since reserves are base money held by banks. Even the electronic reserves held at the Fed (in the Fed's computers I guess) are property of the Fed deposit holders (banks, Tsy, etc). But then you know all that... just thought I'd restate it for other readers!

BTW, Happy New Year Vincent!

I know you like to think about Japan. You might like this:

http://macromarketmusings.blogspot.com/2013/12/how-is-abenomics-doing.html

You might be interested in his preceding article too:

http://macromarketmusings.blogspot.com/2013/12/the-qe-block-versus-emu-block.html

Back to your comments about velocity, Sumner likes to say that MV=QP is really just the definition for V:

V = NGDP/M

But then you probably already knew that too. The way he states that over and over again (see his latest posts), it's as if he's really trying to get people to not think about velocity as a entity in it's own right, but more of a label for the ratio NGDP/M.

Also, it's interesting to see you refer to "inflation" rather than "hyper-inflation" in your post here. Are you de-emphasizing the "hyper" part in your projections? If it's just moderate inflation, will it really be a big concern?

I'll check back at Beckworth's page to see if you made any comments!

All right, have a good one Vincent!

Also, Nick Rowe has had some interesting recent articles about banks, "backed" money and tolerance for nominal risk.

... I made a mistake in the above... electronic Fed deposits held by Tsy are NOT reserves of course. Only base money owned by commercial banks are reserves, by definition.

Delete... and in a flagrant act of self promotion, here's my best summary of "where reserves can go" (for anyone that's interested):

http://brown-blog-5.blogspot.com/2013/04/the-three-places-reserves-can-go.html

I changed it to say "high inflation" as that is really what I meant. Thanks.

DeleteI also put in something about how banks can withdraw their excess reserves as paper money, which has no restrictions on it, so there is no restriction on what they can do with excess reserves. To try to cut you guys off at the pass. Thanks.

I really wish I could find someone who was at least trying to measure relative velocity of money from year to year, as apposed to just calculating it from the other things in the equation of exchange. I think a big bank or Western Union or even a big store like Walmart could record all the notes they see and note how often they saw repeats and make some real index of the velocity of money. It could at least be something we could compare from year to year. This idea would only work for paper money, but it would at least be something.

Here is a paper on measuring the velocity of money that looks interesting. Just starting it so can not say for sure.

Deletehttp://www.lse.ac.uk/economicHistory/pdf/FACTSPDF/1306Morgan.pdf

Nick touches on velocity in this one:

Deletehttp://worthwhile.typepad.com/worthwhile_canadian_initi/2014/01/media-of-exchange-and-the-clearing-house.html

Interesting one. I posted a comment there.

DeleteCullen has a post on monetary base not causing inflation:

http://pragcap.com/inflation-does-not-appear-to-be-monetary-base-driven

I put a $100 reward for a historical example of rapid monetary base expansion without inflation at the end of the above post.

You should email that $100 contest to Marcus Nunes. I posted it on David Glasner's, David Beckworth's (where it didn't show up), and JP Koning's sites. (as I recall posts mentioning you or your blog don't show up on Nune's blog).

DeleteRegarding the velocity bit on Rowe's site, did you see the part where he mentioned the settlement frequency? If continuous I think he said the velocity of "base money" goes up. As the period between settlements goes to infinity, velocity goes to zero (with certain assumptions).

Delete"I will pay $100 US by paypal to the first person to comment below about a case where a central bank increased the monetary base by a factor of 4 or more in 5 years or less and did not get at least double digit inflation sometime during the 5 years after. Must provide links to reliable info on central bank balance sheet expansion and subsequent inflation."

ReplyDeleteThe Reserve Bank of New Zealand increased the monetary base from $3b in autumn 2004 to $12.8b in December 2006. Inflation in NZ never rose above 5% or so in the ensuing 5 year period.

Balance sheet data: http://www.rbnz.govt.nz/statistics/tables/r2/

Inflation data: http://www.rbnz.govt.nz/statistics/key_graphs/inflation/

JP, way to go with the early entry! ... Vincent, did anybody get back to you faster than JP? Vincent, do you have a winner?

DeleteBTW, JP: I posted Vincent's contest in the three most likely places to win (that I'm aware of!), excluding Mark A. Sadowski, whose email I don't have and who doesn't have a blog (AFAIK). I figured it would most likely come down to a contest between you and Mark (I figured Mark would come across it pretty quick). I didn't bother posting at Nunes' because although he's a contender, as I recall any mention of Vincent on there or his blog ends up in spam (but not because Nunes blocked him). I figured Vincent would have time to email Marcus (both of us have his email I think)... and perhaps Vincent did that. I figured Glasner would have a shot or Beckworth, but I figured they might be the underdogs.

Delete:D

Well congratulations! I hope it works out and that Vince will be satisfied with your response. I'm not even going to check :D

Vince, maybe you should have spread that $100 out into several prizes... perhaps there are more examples to be had that people aren't motivated to find now. :D

DeleteJP is first to submit an entry. I am trying to understand the link and the spreadsheet at that link. I find it completely implausible that New Zealand had only $3 billion as a monetary base anytime in the last 100 years. I don't see that claim nor the 12.8 yet either. So I am not sure if we have a winner but I have my doubts so far. Still trying to understand. JP, where exactly are your numbers coming from?

DeleteI can find evidence that New Zealand had $3 billion in M0 in 2004. I can't find evidence that New Zealand had $12.8 billion in M0 in 2006. So I too could use some help reading and understanding the R2 spreadsheet.

Delete"JP, where exactly are your numbers coming from?"

ReplyDeleteI got these numbers from the xls spreadsheet at the top of the first link. To get the monetary base I summed together "Currency in circulation" and "Deposits incl. in monetary base".

Double check my numbers though, I could be wrong. If I do win, Tom gets a finder's fee ;)

The total liabilities goes from 11,322 in Dec 2004 to 20,702 in Dec 2006. The Fed has their balance sheet up by over a factor of 4. This seems like a bit under a factor of 2. It is not obvious to me what should count as monetary base though.

DeleteStill not sure on this one and will judge it under the rules at the time of the entry.

I have changed the rules for future entries a bit. Looking for established central bank and currency where the central bank monetizes so much local government debt that it makes the monetary base go up by a factor of 4 in 5 years or less. So a currency board, or new currency, would not count. Looking for something like the US situation that did not get double digit inflation.

So you took Nov 2004 with currency 3030 and deposits in monetaray base of 2 to add to 3032. Then Dec 2006 these are 3958 and 8886, adding to 12,844. This would be a factor of 4.

DeleteThink we could get Mark to be the judge on what counts as monetary base?

"So you took Nov 2004 with currency 3030 and deposits in monetaray base of 2 to add to 3032. Then Dec 2006 these are 3958 and 8886, adding to 12,844. This would be a factor of 4."

DeleteYep, that's how I did it.

"Think we could get Mark to be the judge on what counts as monetary base?"

Sure, sounds like a good idea.

Tom, can you put up the bat signal for Mark? :-)

DeleteFinder's fee! ... OK, now I'm officially pulling for you JP. :D

DeleteI will give Mark a $20 judges fee.

DeleteTom Brown left a rather cryptic comment for me at The Money Illusion. It was only after reading his comment at Uneasy Money that I figured out what was going on.

DeleteJP Koning is correct. A simpler way of verifying this is to look at Table R3 which clearly labels the amount of the monetary base:

http://www.rbnz.govt.nz/statistics/tables/r3/

I wish someone had told about the contest, I'm actually very hard up for cash right now.

P.S. I'm also not certain this is the only example. I'd have to give this some thought first and see what I can come up with.

I'm willing to have first prize be $50, second prize, $x, and third price $y, for scholarship's sake (as long as Vincent doesn't mind splitting up the $100 in a few different chunks). The more examples we rustle up the more larnin' we all get.

DeleteAfter researching the issue, I think New Zealand is the only easily verifiable example of this occuring (so far). There may be historical examples, or examples of developing nations, but then we get into quality of the data issues.

DeleteInterestingly, by my count there are five very recent cases of quadrupling of the monetary base (monthly average) in five years or less which so far have not had (year on year) double digit inflation:

1) Sweden - November 2009

2) Iceland - March 2010

3) Switzerland - September 2011

4) UK - September 2012

5) US - August 2013

Note that Iceland last had year on year double digit inflation in September 2009, so given the wording of the challenge ("...sometime during the 5 years after...") it will satisfy the requirements if five years passes without double digit inflation. Note also that the US only made the quadrupling of its base by the skin of its teeth, and only if one uses the unadjusted base (SBASENS).

P.S. Do I actually get $20 for judging this? It will buy 6-weeks worth of catfood. (He's a large cat and if I only feed him dry food my life will not be worth living.)

JP, if you are happy with $50 then I propose I also give $50 to Mark and $20 to Tom. I need to know what paypal address to send it to. If you don't want it public here you can email me at vincecate@gmail.com

DeleteIt seems New Zealand expanded by buying Foreign assets. I really want to find one that did it by monetization and so am doing the contest over with another $100 and the fixed up rules above.

Mark, you should do a blog so we would know where to find you!

Did Iceland expand by monetization or something else? I think it is the expansions that can not be unwound that are inflationary. Buying foreign currency can usually be unwound. Buying bonds from a government running huge deficits are not as easy to unwind. The problems are rising interest rates lower the value of the bonds, the government can't get cash if nobody is buying their bonds, and higher interest rates are bad for the economy.

"JP, if you are happy with $50 then I propose I also give $50 to Mark and $20 to Tom."

DeleteSounds good!

I'll try and find an example of a central bank expanding via domestic purchases of bonds, but no modern examples comes to mind at the moment.

"Did Iceland expand by monetization or something else?"

DeleteApproximately 38.9% of the assets the CBI acquired between March 2005 and March 2010 were foreign.

I'm sending you an email with my Paypal address.

Vincent, JP and Mark... just now reading this. Mark I'm glad you tracked this down. I figured you would. I didn't give any names in my "cryptic" comment because I didn't want to bias you either way. :D

DeleteAnd I posted this contest in three places thinking you'd probably see it in one... but JP beat you to it. He was quick! (Of course I posted it directly to his blog).

Congrats JP and Mark (and me, I guess)! Thanks for hosting this game Vincent... it was fun and educational though my contribution was minimal. I would consider giving my $20 to a good cause (like Mark's cat food supply) but given my own finances right now, I think I might need that for cat food myself pretty soon! (Currently my monthly outflow > monthly inflow, which really sucks!)

So ... I looked up my old PayPal account which I haven't used for years, and it's still there! I don't think I ever received a payment via it though (and the funds have long since been drained to $0). So what is the "paypal address?" ... I'll send you an email w/ all the info, but if you need more, don't hesitate. Thanks again all!

Especially you Vincent for running a "clean" game. :D

http://research.stlouisfed.org/publications/review/10/11/Anderson.pdf

Deletewould seem to be relevant...

Yes, see Jan 4th comment below.

DeleteOlde on pragcap found the following interesting study of central bank balance sheet expansion. The summary seems to say it is ok as long as the public believes it will be reversed.

ReplyDeletehttp://research.stlouisfed.org/publications/review/10/11/Anderson.pdf

Note that in every case of hyperinflation the central bank is monetizing lots of debt and getting lots of inflation. So there are lots of historical examples of expanding the base money supply and getting inflation. Expanding and not getting inflation seems the interesting case.

ReplyDeleteFrom the above paper, and the Real BIlls / Backing view of central banks if the central bank expands its balance sheet in a way that it can reverse it, then there need not be any inflation.

ReplyDeleteSo one way to look at this is can the US, UK, and Japanese central banks reverse their balance sheet expansion? I don't think so.

The first round of the contest has been paid as agreed above. I sent $50 to JP, $50 to Mark, and $20 to Tom.

ReplyDeleteA second round of the contest with updated rules is now on for another $100.

Hey Vincent, do you have any theories on deflation? Lars thinks the EuroZone is headed that way:

ReplyDeletehttp://marketmonetarist.com/2014/01/07/one-step-close-to-euro-zone-deflation/

This is the wrong blog for deflation theories. :-) In fiat currencies without any tie to gold the most deflation seems to be Japan, which was not really that much. Inflation and hyperinflation are huge changes in the value of money. Deflation of 1% seems to mostly be an excuse to print more money. I am amazed at how many people are worried about deflation when historically the odds of inflation are so much higher, in pure fiat money. In my hyperinflation FAQ I have a graph showing how deflation and inflation were similar probability things under gold, but since 1971 the odds are just not the same.

Deletedeflation theories: sure you have them! Just run your inflation ones in reverse! :D

Delete38 year cycle ~= pi*12 does this look familiar? :-)

ReplyDeleteStill, no hyperinflation in the US, unless it goes into complete isolation (think iron curtain) from the world, lose its technological/industrial status #1, lose its demographic advantage, lose it's tremendous energy advantage, etc, etc. With all the head winds and drawbacks, the US will be the last man standing :-) :-)

Joe 6-pack

My rebuttal to Vince's comments... Don't expect any inflation at all. Expect low growth for a while.

ReplyDeletehttp://sucesofinanciero.blogspot.com/2014/01/response-to-vince-cate-at-how-fiat-dies.html

I have replied on that blog.

DeleteBack at you...

Deletehttp://sucesofinanciero.blogspot.com/2014/01/response-to-vince-cate-at-how-fiat-dies.html

Vincent, I thought you might like this one from Nick Rowe:

ReplyDeletehttp://worthwhile.typepad.com/worthwhile_canadian_initi/2014/01/monetary-policy-fiscal-policy-the-target-and-the-size-of-the-central-bank.html

Here's a good quote:

"As we lower the inflation target (or NGDP level growth target), the demand for the central bank's currency would increase, the average size of the central bank would increase, relative to GDP, and so would the absolute size of those fluctuations in size."

Scott Sumner contributes as well in the comments:

"This is a point I am also trying to make. And the implication is that the actual "zero lower bound" is not zero rates, it's when you reach "zero eligible assets left to buy."

Regarding the "extreme socialists," I like to sometimes tease conservatives who want really low inflation by pointing out that that they are advocating socialism."

So if you want 0% inflation, you must be an extreme socialist. :D

Most conservatives have no clue about the economy. The libertarians are the ones that will really destroy the socialists - ask them what rate of inflation they want.

DeleteWell, I will answer that one for you. Inflation is not necessarily an increase in prices. But, higher prices are a symptom of inflation. Inflation is simply an increase in the amount of money and credit. Any amount of money supply + credit would do - but that does not mean prices will not increase. Prices can in fact increase due to many factors outside of the money supply, like weather, diseases, natural disasters, etc..

Socialists are those that are all in for handouts, and all out for producing those things they want to hand out. Let's see, everyone should line up to get free food, education, homes, clothing - and nobody lines up to produce them. Does that make sense to you? I don't think so.

Vanessa A,

DeleteSumner calls himself a "practical libertarian" and he doesn't care about inflation at all. He thinks the fact that world central banks and governments currently ARE concerned with inflation is a colossal problem. He thinks that CBs should forget about inflation and start explicitly targeting NGDP levels (the practice knows as NGDPLT). He points out that once CBs started targeting inflation back in the late 70s and early 80s in the developed world (Fed, BoC, BoJ etc) that inflation has ceased to be a problem in those countries, except that it sometimes gets too low (and that's only because those CB's lose their nerve to maintain the target during recessions).

He argues that NGDPLT is more "conducive to macro stability" than I.T. (see my Sumner quote in the comment below), so inflation should be completely dropped as a CB target.

And he's far from the only (self proclaimed) libertarian in this camp: e.g. Lars Christensen, Marcus Nunes, David Beckworth and Bill Woolsey are some other libertarian economists that share this view. Glasner and Rowe may or may not be libertarians, but they too share it.

Regarding inflation, I believe most economists (left, right, center and libertarian) mean growth of price level by that. All the economists in the above list will answer your questions on their blogs, so I encourage you to check with them. In fact try other non-libertarian, non-Market Monetarist economists: Noah Smith, Stephen Williamson, John Cochrane, Brad DeLong.... I'll bet you'll have trouble finding an opinion too far from Sumner's on this. Unless you ask an Austrian I guess. Ha! I don't follow them, so I don't know.

Defining "inflation" as growth in the base money supply is the trick that Peter Schiff uses to explain away his failed hyperinflation predictions over the past 5 years. Kudlow challenged him on these failed predictions to which he essentially responded "But my definition of inflation doesn't have anything to do with price levels: it is only about the quantity of base money, so my predictions were all correct!!" The incredulous Kudlow then mocked him "So for five years you've been giving dire warnings that if the Fed creates more base money, then there'll soon be more base money??? Lol!" To which Schiff essentially said "Yes." (I'm paraphrasing). :D

I'm guessing you're not a Schiff fan (because I'm sensing you're a Mish fan instead?) and probably not a hyperinflationist (otherwise, why would you be here arguing against Vincent's hyperinflation warnings?), but your definition of inflation seems to overlap with that of Schiff's which seems to me to be tailor made to help Schiff save face during TV interviews.

... though in fairness, on re-reading Rowe's piece, I think he's saying that targeting inflation OR NGDP levels too low (close to 0) will force the CB to be large (and is thus the "socialist" option, Ha!).

DeleteVincent, I also thought you might like this one from Scott Sumner, at least the last bit where he brings up the gold standard:

ReplyDelete"It’s really, really hard to cheat on level targeting. That’s why central banks don’t do it, it gives them very little discretion and they know it. And that’s exactly why I like it. It’s really effective, for better or worse. The gold standard was sort of like that, but with a target (gold prices) that was much less conducive to macro stability than NGDP."

http://www.themoneyillusion.com/?p=25823

How do you explain the deflationary forces building in Europe and soon to be in Emerging markets as debt implodes. Does deflation not get exported to North America. What stops this process? Are we going to see deflation first?

ReplyDeleteAlso, rising interest rates with inflation will affect equities and end the asset inflation, will it not?

When banks loan out demand deposits they make it seem like there is more money since both the guy who now has the money and the person who has the demand deposit think they can spend the money. So you can theoretically get deflation if people are paying down loans faster than new loans are being made. But with governments all running huge deficits it is mostly theoretical. Sometimes there is a bit of deflation right before hyperinflation. Eventually the rate of printing new money overpowers any loan payoffs going on. Don't know if we will actually see prices go down.

DeleteYes, with rising inflation and rising interest rates I would expect to see stocks, bonds, and real estate go down, at least at first. The bond bubble should really pop.

In order to get high inflation, you have to increase *consumer* prices. In order to get higher consumer prices, you have to give consumers money to chase those prices. In order to increase wages, unemployment has to fall. For unemployment to fall, GDP will pretty much have to increase.

ReplyDeleteYou get to choose your definition of money supply and price level. But it's kinda important that you choose correct relevant pairs. M2 and M3 are still growing on the order of 5% a year, and those are the values that are going to have to spike in order to produce serious demand-shock inflation.

When consumers are going into hyperinflation what they pay for necessities goes up much more than their salaries. Life gets hard under hyperinflation. The way this is possible is they have to cut back on non-necessities. Some things that you might think of as necessities, like rent, are not really as you can move in with relatives.

DeleteNominal GDP does go up going into hyperinflation.

As the velocity of base money goes up, then m2 will be going up. The reason it can spike up is that the velocity is not under the control of the central bank or government.

Look at Japan. The prices for food and other imports are going up much faster than the consumer salaries. The shock seems to come from the exchange rate going down. Foreigners drive up the price of exports and imports are directly more expensive. This provides a price shock to the economy, not a demand shock.