There have been many econoblog posts of the form, "ha, ha, the people predicting inflation have been wrong so far, when will they give up?". Let me try to explain why we know high inflation is coming eventually.

The

equation of exchange shows the relationship between the money supply, velocity of money, price level, and real GNP. This equation is a tautology that no competent economist would argue against.

Money-supply * Velocity-of-money = Price-level * Real-GNP

On the scale that we are currently increasing the money supply, the real GNP is basically constant. Inflation can be thought of as

too much money chasing too few goods. When looking at a 400% change in the base money supply over the last 5 years, the change in real GNP (change in goods) is so small that we won't be off much by ignoring it. To help understand this short period of time with a big change in the base money supply, we can make a simplified version of the equation of exchange.

Money-supply * Velocity-of-money = Price-level * constant

If the velocity goes down as the money supply goes up, it is possible to increase the money supply without changing the price level.

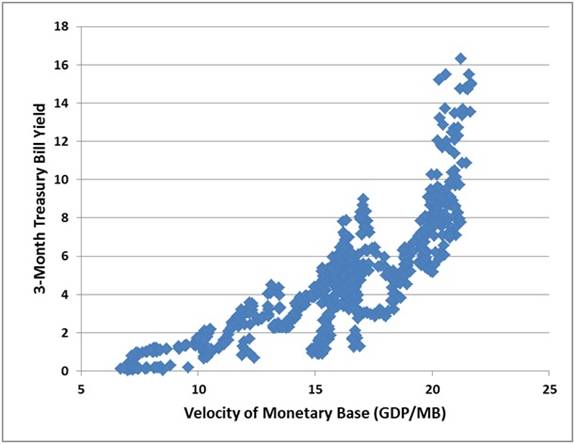

Hussman has shown that as interest rates go down the velocity of money goes down and as interest rates go up the velocity of money goes up.

At first when the Fed makes new money and buys bonds, they increase the price of bonds, which means they lower the interest rate. Hussman's data shows this lowers the velocity of money. The lower velocity can compensate for the increased quantity of money so that often new money does not cause inflation right away.

The equation of exchange can be used with whichever definition of money supply you want to use (base money, M1, M2, etc). It is most clear that inflation will come if we

use

base money as our definition of the money supply. The base money supply has gone up by around a factor of 4 in about 5 years.

Since we have so far avoided inflation, the velocity of base money must have gone down by about a factor of 4 during this same period. The way this happened is that most of the new base money the Fed has made has just sat still in the Fed as

excess reserves. This huge amount of non-moving money lowers the overall average velocity of money. If you think about it, it makes sense that making new money that does not leave the Fed should not cause inflation. Paying higher interest on excess reserves than short term bonds were paying was

Bernanke's great new trick to hide a few trillion dollars out in the open.

However,

now interest rates are going up. From Hussman we should now expect the velocity of money to go up. From the simplified equation of exchange, when the velocity of money and the money supply are both going up we should expect inflation.

As interest rates return to normal levels, the velocity of money will also return to normal levels. Then we will have 4 times the money supply and a normal velocity of money. By the simplified equation of exchange, we will then have 4 times the price level. We will have very high inflation.

You may be wondering, "why can't the Fed hold interest rates down forever?". Good question. If inflation is higher than the interest rate, then everyone and their brother can make money by borrowing and buying random stuff. To hold rates down the Fed would have to make an ever increasing amount of money, resulting in ever increasing inflation and ever increasing borrowing. The Fed seems interested in tapering their money creation which will mean letting interest rates go up. Japan, at least for the moment, seems to have chosen to try to hold interest rates down no matter how much money creation it takes. Once government debt and deficit are out of control, there is no good path for the central bank.

For the velocity of money to return to normal, it is reasonable to expect the excess reserves at the Fed will enter the real economy. There are those who think these excess reserves are somehow trapped but a bank with excess reserves can send an armored truck to the Fed and withdraw paper Federal Reserve Notes with no restrictions on them. This could happen at any time and possibly very suddenly. A couple trillion dollars suddenly flowing into the real economy would clearly result in high inflation.

Even Krugman has said that

increasing the money supply is only safe when interest rates are near the zero lower bound. With interest rates going up, even by Krugman's logic, we should expect inflation.

Here is another way to look at it. From 1913 to 2007 the Fed made about $800 billion in new money total. Since then it makes around that much each year. Nearly 94 years worth of money every 12 months. In this environment, one should expect to see "too much money chasing too few goods".

Another way to look at it. In order to not cause inflation the central bank would need to be able to withdraw all the new money they created. There is just no way this can happen. Interest rates would shoot up, the value of the bonds the Fed held would crash, and they could not sell them for enough to withdraw as much money as they created.

High inflation will come. It is just a question of when.

Prize for historical example of 4x on monetary base and low-inflation

There are more than 100 cases where rapid monetization seems to have resulted in

hyperinflation (using 26% cutoff). I am looking for one good example where it did not.

I will pay $100 US by paypal to the first person to comment below about a case where a central bank increased the monetary base by a factor of 4 or more by buying government bonds in 5 years or less and did not get at least double digit inflation sometime during that time or the 5 years after. Must provide links to reliable info on base money growth and subsequent inflation.

This has to be for an established central bank, not a new one or a new currency at an old one (currency and bank around for at least 10 years prior to 4x period). It must be expanding the monetary base by buying up government bonds for that country (like US, UK, and Japan are doing). I am looking for a situation where a central bank did something similar to what the US has done in the last 5 years but that did not get high inflation.

Note one round of this has been won as of 1/5/14 (see comments) but I had not specified that the 4x expansion had to be from monetization which is in the current rules.

All

it would take is for one case where the equation of exchange did not

work. One time where the interest rates and inflation rates went up

substantially but the velocity of money did not. One historical case

where a central bank bought up half of a government debt that was more

than 100% of GNP, using new made money, without getting serious

inflation in the next 10 years. Maybe that is your answer, 10 years.

But I don’t think it has ever happened in history and there are many

many many times where lots of new money caused inflation down the road.

You have to think “this time is different” to not expect inflation at

some point. Doubt it very much.

Read more at

http://pragcap.com/my-favorite-posts-from-2013#p4TCJp3CbFyzp1OI.99

All

it would take is for one case where the equation of exchange did not

work. One time where the interest rates and inflation rates went up

substantially but the velocity of money did not. One historical case

where a central bank bought up half of a government debt that was more

than 100% of GNP, using new made money, without getting serious

inflation in the next 10 years. Maybe that is your answer, 10 years.

But I don’t think it has ever happened in history and there are many

many many times where lots of new money caused inflation down the road.

You have to think “this time is different” to not expect inflation at

some point. Doubt it very much.

Read more at

http://pragcap.com/my-favorite-posts-from-2013#p4TCJp3CbFyzp1OI.99

All

it would take is for one case where the equation of exchange did not

work. One time where the interest rates and inflation rates went up

substantially but the velocity of money did not. One historical case

where a central bank bought up half of a government debt that was more

than 100% of GNP, using new made money, without getting serious

inflation in the next 10 years. Maybe that is your answer, 10 years.

But I don’t think it has ever happened in history and there are many

many many times where lots of new money caused inflation down the road.

You have to think “this time is different” to not expect inflation at

some point. Doubt it very much.

Read more at

http://pragcap.com/my-favorite-posts-from-2013#p4TCJp3CbFyzp1OI.99

I’d love to go back and forth on this stuff, but I am pretty busy today so maybe another time. Take care.